- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Perp DEX Showdown: Who Is the Winner?

Original Article Title: The Perp DEX Wars of 2025: Hyperliquid, Aster, Lighter, and EdgeX

Original Article Author: @stacy_muur

Translation: Peggy, BlockBeats

Editor's Note: The decentralized perpetual contract exchange (Perp DEX) track has undergone drastic changes in the past year: from Hyperliquid's absolute dominance to the rise of Aster, Lighter, and EdgeX, the market landscape is being reshaped.

This article provides an in-depth analysis of the four major platforms from the perspectives of technical architecture, key metrics, risk events, and long-term viability, aiming to help readers see the "truth behind the data" rather than relying solely on trading volume rankings.

The following is the original article:

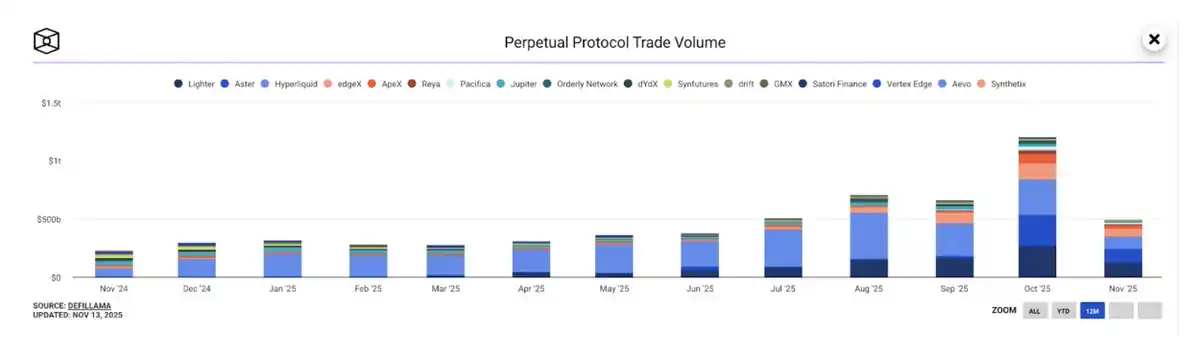

In 2025, the decentralized perpetual contract (perp DEX) market experienced explosive growth. In October 2025, the monthly trading volume of perpetual contract DEX surpassed $12 trillion for the first time, quickly attracting high attention from retail traders, institutional investors, and venture capital funds.

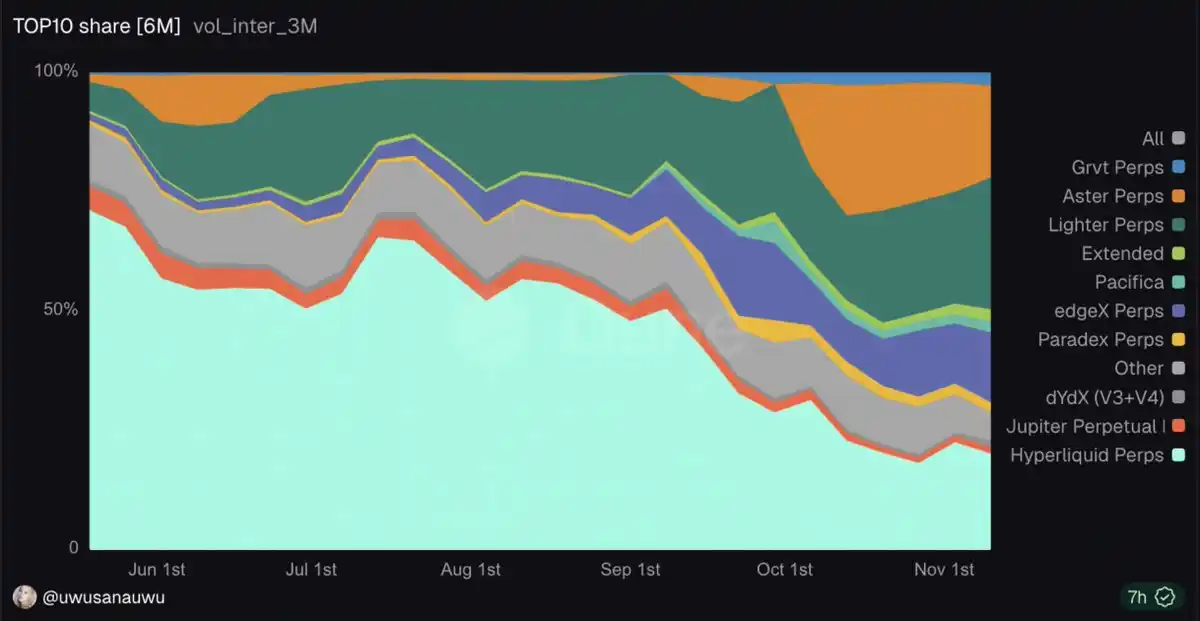

Over the past year, Hyperliquid almost monopolized the lead, reaching its peak in May this year, occupying 71% of on-chain perpetual contract trading volume. However, by November, its market share had plummeted to only 20%, with emerging competitors quickly seizing territory:

- Lighter: 27.7%

- Aster: 19.3%

- EdgeX: 14.6%

In this rapidly evolving ecosystem, the four dominant players have already emerged, engaging in fierce competition for industry dominance:

@HyperliquidX – The veteran champion of on-chain perpetual contracts

@Aster_DEX – The massive trading volume, controversy-ridden "rocket"

@Lighter_xyz – The disruptor with zero fees and native zk

@edgeX_exchange – The "dark horse" quietly aligned with institutions

This in-depth investigation aims to dispel the fog, dissecting the technical strength, key metrics, controversial focus, and long-term viability of each platform.

Part 1: Hyperliquid, the Undisputed Champion

Why Hyperliquid Reigns Supreme

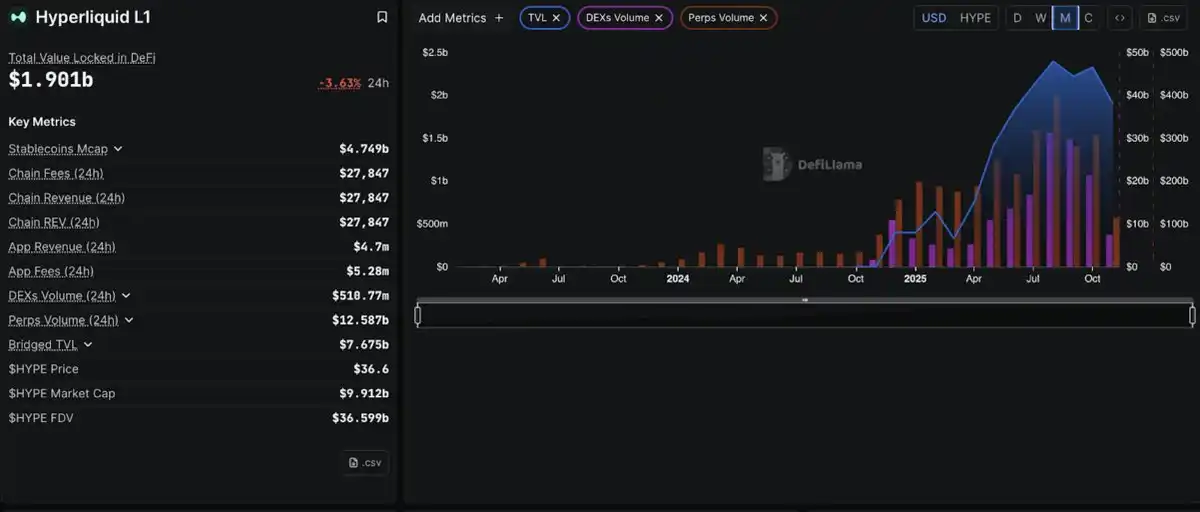

Hyperliquid has solidified its position as the industry-leading decentralized perpetual contract trading platform, with a peak market share exceeding 71%. Despite competitors grabbing headlines with explosive trading volume growth, Hyperliquid remains a foundational pillar of the entire perpetual contract DEX ecosystem.

Technological Foundation

Hyperliquid's advantage stems from a revolutionary architectural decision: creating a custom Layer 1 blockchain designed specifically for derivative trading. Its HyperBFT consensus mechanism achieves sub-second order confirmation and supports 200,000 transactions per second, performance comparable to or even surpassing centralized exchanges.

The Truth About Open Interest

Competitors often attract attention with astounding 24-hour trading volumes, but the true indicator of capital deployment is Open Interest (OI), which represents the total value of all perpetual contracts still held.

Trading volume indicates activity, while Open Interest indicates capital commitment.

According to 21Shares data, as of September 2025: Aster occupies approximately 70% of total trading volume; Hyperliquid temporarily dropped to around 10%

However, this is only a volume advantage, and trading volume is the most easily manipulated metric through incentives, rebates, market maker frequent trading, or even "wash trading" behavior.

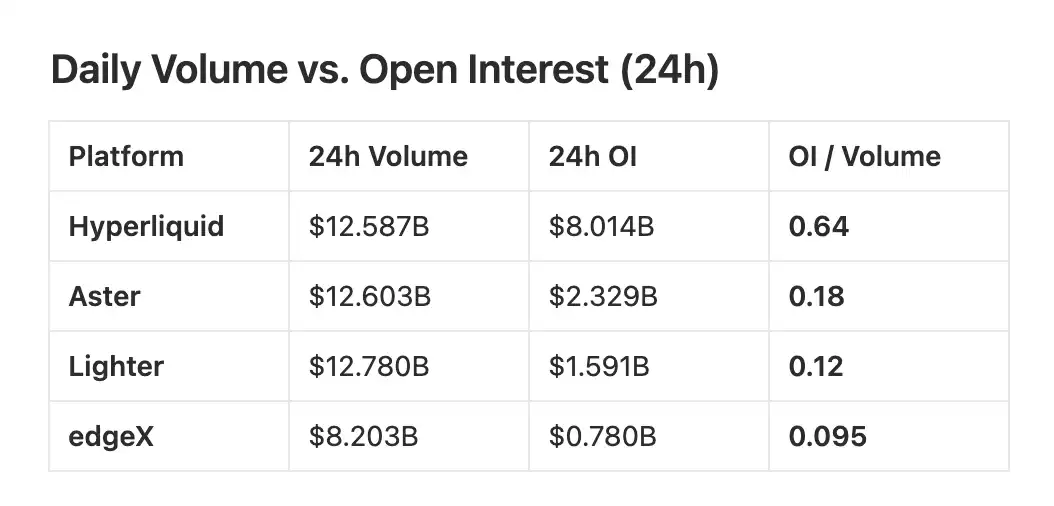

The latest 24-hour Open Interest data shows:

-Hyperliquid: $8.014B

-Aster: $2.329B

-Lighter: $1.591B

-edgeX: $780.41M

Total OI for the top four platforms: $12.714B

Hyperliquid's share: approximately 63%

This means that Hyperliquid holds nearly two-thirds of the entire market's Open Interest, surpassing the combined total of Aster, Lighter, and edgeX.

Open Interest Market Share (24h)

- Hyperliquid: 63.0%

- Aster: 18.3%

- Lighter: 12.5%

- edgeX: 6.1%

This metric reflects traders' willingness to hold funds overnight rather than purely for incentive mining or high-frequency trading.

Hyperliquid: High OI/Volume ratio (around 0.64), indicating a significant amount of trading volume translating into sustained open positions.

Aster & Lighter: Low ratios (around 0.18 and 0.12), suggesting frequent trading but minimal fund retention, typical of incentive-driven behavior rather than stable liquidity provision.

Full Picture

Trading Volume (24h): Indicates short-term activity

Open Interest (24h): Indicates retained risk capital

OI/Volume Ratio (24h): Reveals genuine trading vs incentive-driven trading

Across all OI-related metrics, Hyperliquid emerges as the structural leader: highest open interest; largest share of committed funds; strongest OI/Volume ratio; total OI exceeding the sum of the latter three platforms

While trading volume rankings may fluctuate, open interest unveils the true market frontrunner, which is Hyperliquid.

Real-World Validation

During the liquidation event in October 2025, $190 billion in positions were liquidated, and Hyperliquid maintained zero downtime during the peak trading volume.

Institutional Recognition

21Shares has submitted the Hyperliquid (HYPE) product application to the U.S. SEC and listed a regulated HYPE ETP on the Swiss stock exchange. These developments (including coverage on platforms like CoinMarketCap) indicate increasing institutional access to HYPE. The HyperEVM ecosystem is also expanding, although public data has not yet validated claims of "180+ projects" or "$4.1B TVL."

Conclusion

Based on the current record-keeping, exchange listings, and ecosystem growth, Hyperliquid demonstrates a strong momentum and increasing institutional recognition, further solidifying its position as a leading DeFi derivatives platform.

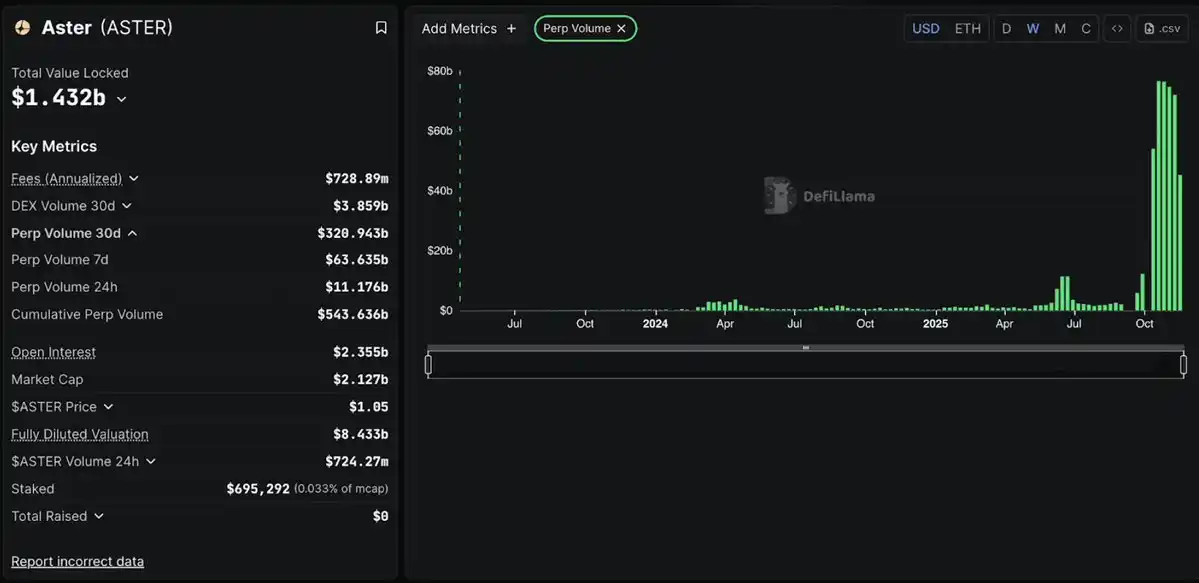

Part 2: Aster, Explosive Growth Amid Controversy

Aster's Positioning

Aster is a multi-chain perpetual contract trading platform that launched in early 2025 with a clear goal: to provide users with high-speed, high-leverage derivative trading on networks such as BNB Chain, Arbitrum, Ethereum, and Solana without the need for cross-chain asset transfers.

The project did not start from scratch but rather originated from the merger of Asterus and APX Finance at the end of 2024, combining APX's mature perpetual contract engine with Asterus's liquidity technology.

Explosive Rise

Aster launched on September 17, 2025, at $0.08 and skyrocketed to $2.42 in just one week, a staggering 2800% increase. The daily trading volume surged past $700 billion at its peak, temporarily dominating the entire perpetual contract DEX market.

The fuel for this "rocket"? CZ. The founder of Binance supported Aster through YZi Labs and personally tweeted to boost it, causing the token's price to soar. In the first 30 days of trading, Aster's cumulative trading volume exceeded $320 billion, briefly capturing over 50% market share.

DefiLlama Delisting Incident

On October 5, 2025, as the most trusted data source in the crypto industry, DefiLlama delisted Aster's data due to its trading volume being nearly identical to Binance's trading volume (1:1 correlation).

Real trading platforms exhibit natural fluctuations, and perfect correlation only means one thing: data manipulation.

Evidence includes:

- Trading volume patterns perfectly synchronized with Binance (across all pairs like XRP, ETH, etc.)

- Aster's refusal to provide trading data, making it impossible to verify the authenticity of trades

- 96% of ASTER tokens concentrated in 6 wallets

- Transaction Volume/OI Ratio as high as 58+ (Healthy level should be below 3)

ASTER token immediately dropped by 10%, from $2.42 to approximately $1.05

Aster's Defense

CEO Leonard claimed that this correlation was only due to "airdrop users" hedging on Binance. But if true, why refuse to provide public data as proof?

Weeks later, Aster relisted, but DefiLlama warned: "It's still a black box, we can't verify the data."

Its Actual Offerings

To be fair, Aster does have some technical highlights: 1001x leverage; hidden orders; multi-chain support (BNB, Ethereum, Solana); stakable collateral

Furthermore, Aster is building the Aster Chain based on zero-knowledge proofs for privacy protection. However, even great technology cannot cover up fake metrics.

Conclusion

Concrete evidence:

- Perfect correlation with Binance = Wash trading

- Lack of transparency = Concealment of facts

- 96% token concentration = High centralization

- DefiLlama delisting = Reputation collapse

Aster captured significant value through CZ's hype and fake trading volume but failed to establish a real infrastructure. Perhaps surviving due to Binance support, its reputation has been permanently damaged.

To Traders: High risk, you are betting on CZ's narrative, not real growth. Please set strict stop losses.

To Investors: Avoid, too many red flags, there are better options in the market (e.g., Hyperliquid).

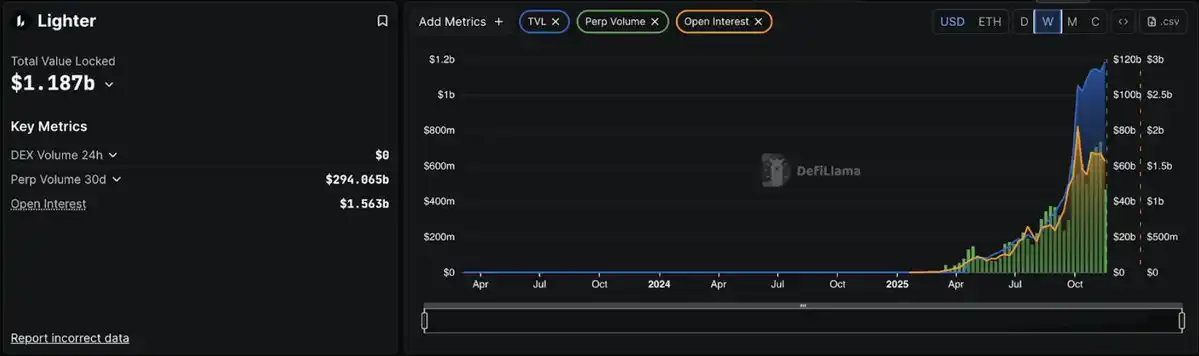

Part Three: Lighter, Impressive Tech, Doubtful Metrics

Technological Advantages

Lighter is unique. Founded by a former Citadel engineer and backed by Peter Thiel, a16z, and Lightspeed (raised $68 million, $15 billion valuation), its core technology involves encrypting every transaction using Zero-Knowledge Proofs (ZK).

As an Ethereum Layer 2 (L2), Lighter inherits Ethereum's security through an "escape hatch" mechanism—even if the platform fails, users can still retrieve funds via smart contract. Application chains on L1 do not have this security feature.

Lighter launched on October 2, 2025, and within weeks, its TVL surpassed $11 billion, with a daily trading volume of $70-80 billion and over 56,000 users.

Zero Fees = Aggressive Strategy

Lighter charges 0 fees for both Maker and Taker transactions, completely disrupting the decision-making of fee-sensitive traders.

The strategy is simple: to capture market share through an unsustainable economic model, build user loyalty, and subsequently achieve profitability.

October 11 Stress Test

10 days after the mainnet launch, the crypto market experienced its largest liquidation event in history, with $190 billion in positions liquidated.

Good news: The system remained operational during a 5-hour turmoil, with LLP providing liquidity as competitors retreated.

Bad news: The database crashed after 5 hours, leading to a 4-hour platform outage.

Worse news: LLP incurred losses, while Hyperliquid's HLP and EdgeX's eLP were profitable.

Founder Vlad Novakovski explained: The original plan was to upgrade the database on Sunday, but the intense Friday fluctuations prematurely crippled the old system.

Volume Manipulation

Data strongly suggests wash trading behavior:

- 24-hour trading volume: $127.8 billion

- Open interest (OI): $15.91 billion

- Volume/OI ratio: 8.03

- Healthy range = below 3, suspicious above 5, 8.03 is extremely abnormal.

Comparison:

Hyperliquid: 1.57 (Natural)

EdgeX: 2.7 (Moderate)

Aster: 5.4 (Concerning)

Lighter: 8.03 (Severe wash trading)

For every $1 deployed by traders, $8 in trading volume is generated—indicative of frequent flipping for wash trading, not actual positions held.

30-day data validation: $2.94 trillion trading volume vs. $470 billion cumulative OI = 6.25 ratio, still significantly above a reasonable level.

Airdrop Question

The Lighter loyalty program is highly aggressive. Loyalty points will be converted to LITER tokens at TGE (expected in Q4 2025/Q1 2026). The OTC market values points at $5-100+, with a potential airdrop value of tens of thousands of dollars, explaining the explosive trading volume.

Key question: What will happen after TGE? Will users stay or will trading volume collapse?

Conclusion

Advantages:

Cutting-edge technology (ZK verification in place)

Zero fees = a true competitive advantage

Inherited Ethereum security

Top-tier team with capital backing

Concerns:

8.03 transaction volume/OI ratio = severe wash trading

LLP incurred losses in stress testing

4-hour downtime raised questions

Post-airdrop user retention not validated

Key difference from Aster: No wash trading accusations, no DeFiLlama delisting. The high ratio reflects aggressive but temporary incentives, not systematic fraud.

Bottom Line Assessment: Lighter boasts world-class technology but is shrouded in suspicious metrics. Can they convert wash traders into real users? Tech says "can," history says "maybe not."

To wash traders: Good opportunity before TGE.

To investors: Wait 2-3 months after TGE, observe if trading volume sustains.

Probability assessment: 40% become a top-three platform, 60% devolve into another "wash farm," just with better underlying technology.

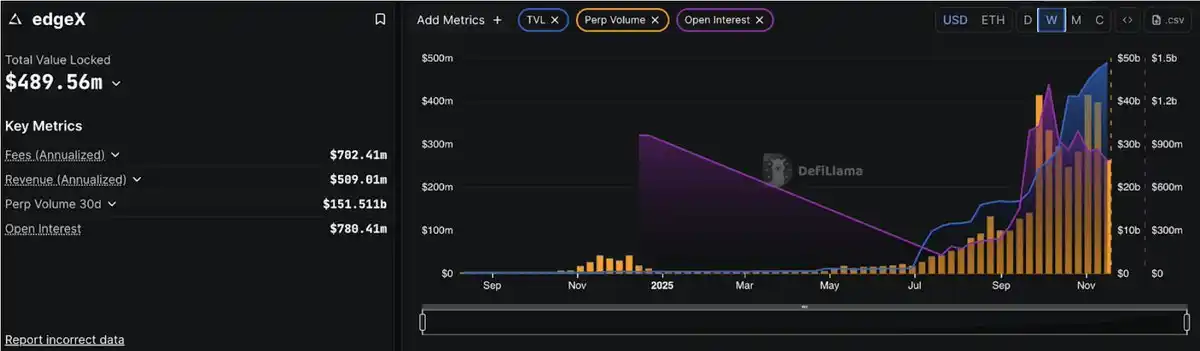

Part Four: EdgeX, Institutional-Grade Pro Player

Amber Group's Advantages

EdgeX operates differently. It originates from Amber Group's incubator (managing $50 billion AUM), with team members from Morgan Stanley, Barclays, Goldman Sachs, Bybit. This isn't "crypto-native" learning finance but traditional finance (TradFi) experts bringing institutional experience into DeFi.

Amber's market-making DNA directly empowers EdgeX: deep liquidity, tight spreads, and execution quality rivaling centralized exchanges. The platform launched in September 2024 with a clear goal: achieve CEX-level performance without sacrificing self-custody.

Built on StarkEx (StarkWare's mature ZK engine), EdgeX can process 200,000 orders per second, with latencies below 10 milliseconds, on par with Binance's speed.

Lower Fees Than Hyperliquid

EdgeX excels in fees compared to Hyperliquid:

Taker Fee: EdgeX 0.038% vs Hyperliquid 0.045%

Maker Fee: EdgeX 0.012% vs Hyperliquid 0.015%

For a trader with a monthly volume of $10 million, savings can amount to $7,000-$10,000 per year, and at the retail order level (<$6 million), EdgeX offers better liquidity, tighter spreads, and lower slippage.

Real Revenue, Healthy Metrics

Unlike Lighter's zero-fee model or Aster's questionable data, EdgeX has created real, sustainable revenue:

TVL: $4.897 billion

24-Hour Trading Volume: $82 billion

Open Interest (OI): $7.8 billion

30-Day Revenue: $41.72 million (147% QoQ growth)

Annualized Revenue: $5.09 billion (second only to Hyperliquid)

Trading Volume/OI Ratio: 10.51 (seemingly high, but requires in-depth analysis)

At first glance, 10.51 may seem high, but context is crucial: EdgeX initially employed an aggressive incentive program to drive liquidity at launch, and as the platform matures, this ratio is steadily improving. More importantly, EdgeX has maintained healthy revenue during this period, proving the presence of real traders rather than pure wash traders.

October Stress Test

During the market crash on October 11th ($190 billion liquidated), EdgeX performed exceptionally:

No downtime (Lighter had 4 hours of downtime)

eLP Treasury remained profitable (Lighter's LLP suffered losses)

Liquidity Provider Annualized Return Rate 57% (industry-leading)

The eLP (EdgeX Liquidity Pool) demonstrated outstanding risk management capabilities during extreme volatility, remaining profitable while competitors faced difficulties.

EdgeX Differentiation Advantages

Multi-Chain Flexibility: Supports Ethereum L1, Arbitrum, BNB Chain; Collateral supports USDT and USDC; Cross-chain deposits and withdrawals (Hyperliquid limited to Arbitrum).

Best Mobile Experience: Official iOS and Android apps (not available on Hyperliquid), simple interface for easy position management anytime.

Asian Market Strategy: Actively positioning in the Asian market through localized support and participation in Korea Blockchain Week, seizing the region overlooked by Western competitors.

Transparent Incentive Program: 60% Trading Volume, 20% Referrals, 10% TVL/Treasury, 10% Liquidation/OI

Clear Statement: "No volume mining rewards," and the metrics validate this—trading volume/OI ratio is improving, not deteriorating.

Challenges

Market Share: Only accounts for 5.5% of perpetual contract DEX open interest, to grow, more aggressive incentives (risk of score manipulation) or major partnerships are required.

Lack of "Killer Feature": EdgeX performs well in all aspects but lacks disruptive innovation, presenting itself as a "business-class" option, professional but not dazzling.

Unable to Compete with Lighter on Fees: Zero fees make EdgeX's "lower than Hyperliquid" advantage less attractive.

Late TGE Timing: Expected in Q4 2025, missing out on the initial airdrop frenzy.

Conclusion

EdgeX is the choice for professional users—reliability triumphs over flashiness.

Advantages:

Amber Group institutional support

$5.09 billion annual revenue

Treasury profitability in stress tests, APY up to 57%

Fees lower than Hyperliquid

No volume mining scandals, clean metrics

Multi-chain support + Best mobile experience

Concerns:

Small market share (5.5% OI)

Trading volume/OI ratio still high (but improving)

Lack of unique selling points

Pressure from zero fee competition

Target Audience:

Asian traders needing localized support

Institutional User, Emphasizing Amber Liquidity

Conservative Trader, Prioritizing Risk Management

Mobile-First User

LP Investor Seeking Stable Returns

Bottom Line Assessment: EdgeX is poised to capture a 10-15% market share in the Asian market, among institutions and conservative traders. It will not threaten Hyperliquid's dominant position, but it doesn't need to—it is building a sustainable, profitable niche market.

Think of it as the "Kraken of Perpetual Contract DEX": Not the largest, not the flashiest, but sturdy, professional, and highly valued by mature users who prioritize execution quality.

For Yield Farmers: Moderate opportunity, less intense competition compared to other platforms.

For Investors: Suitable for small position diversified investments, low risk, low return.

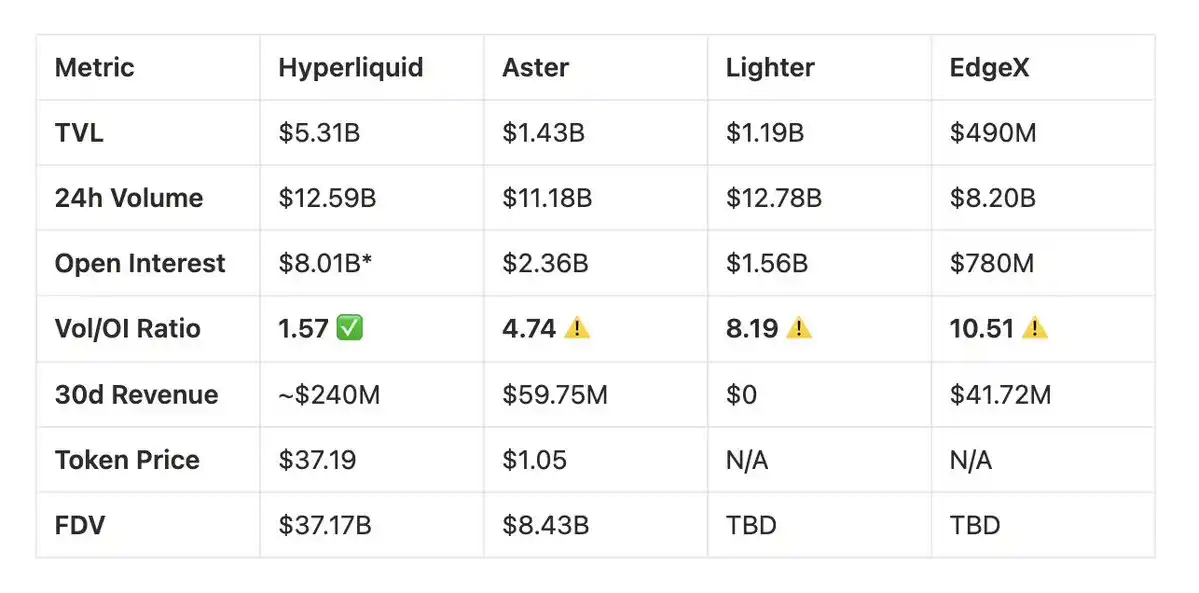

Comparative Analysis: Perp DEX Wars

Trading Volume/Open Interest (OI) Analysis

Industry Standard: Healthy Ratio ≤ 3

Hyperliquid: 1.57 ✅ Indicates a strong organic trading pattern

Aster: 4.74 ⚠️ Slightly high, reflecting significant incentive activities

Lighter: 8.19 ⚠️ High ratio implies incentive-driven trading

EdgeX: 10.51 ⚠️ Points plan impact is evident, but showing improvement

Market Share: Open Interest Distribution

Total Market: Approximately $13B OI

Hyperliquid: 62% - Market Leader

Aster: 18% - Strong Second Tier

Lighter: 12% - Continued Growth

EdgeX: 6% - Focused on a niche market

Platform Overview

Hyperliquid - Seasoned Leader

Controls 62% market share, stable metrics

Annual Revenue $2.9B, active buyback program

Community Ownership Model, Reliable Performance

Advantages: Market Leadership, Sustainable Economic Model

Rating: A+

Aster - High Growth, High Uncertainty

Strong Integration with BNB Ecosystem, CZ Endorsement

Faced DefiLlama Data Scrutiny in October 2025

Multi-chain Strategy Driving Adoption

Advantages: Ecosystem Support, Retail User Coverage

Concerns: Need to Monitor Data Transparency Issues

Rating: C+

Lighter - Technology Vanguard

Zero Fee Model, Advanced ZK Verification

Top-tier Investors (Thiel, a16z, Lightspeed)

Prior to TGE Stage (2026 Q1), Limited Performance Data

Advantages: Technological Innovation, Ethereum L2 Security

Concerns: Business Model Sustainability, User Retention Post Airdrop

Rating: Not Completed (Awaiting TGE Performance)

EdgeX - Institution-driven

Endorsed by Amber Group, Professional-grade Execution

$509M Annualized Revenue, Stable Treasury Performance

Asia Market Strategy, Mobile-first

Advantages: Institutional Reputation, Steady Growth

Concerns: Small Market Share, Competitive Positioning

Rating: B

Investment Considerations

Exchange Selection:

Hyperliquid: Deepest Liquidity, Reliability Validation

Lighter: Zero Fees, Suitable for High-frequency Traders

EdgeX: Lower Fees than Hyperliquid, Excellent Mobile Experience

Aster: Multi-chain Flexibility, BNB Ecosystem Integration

Token Investment Timeline:

HYPE: Now Available, $37.19

ASTER: Trading at $1.05, watch for future developments

LITER: TGE 2026 Q1, metrics to be evaluated post-launch

EGX: TGE 2025 Q4, observe initial performance

Key Takeaways

Market Maturity: Clear differentiation in the Perp DEX space, with Hyperliquid establishing dominance through sustainable metrics and community collaboration.

Growth Strategies: Each platform targets different user demographics—Hyperliquid (Professional), Aster (Retail/Asia), Lighter (Tech), EdgeX (Institutional).

Metrics Focus: Metrics such as Trading Volume/OI ratio and Revenue Generation Ratio can better reflect performance than mere trading volume.

Future Outlook: Post-TGE performance of Lighter and EdgeX will determine long-term competitiveness; Aster's future hinges on addressing transparency issues and maintaining ecosystem support.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.