- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Unstable Stablecoins

Original Title: Stables are not Stable

Original Author: @yq_acc

Translation: Peggy, BlockBeats

Editor's Note: Over the past five years, decentralized finance (DeFi) has experienced a cycle from hype to collapse, with stablecoins being repeatedly proven to be "unstable."

This article takes the November 2025 Stream Finance collapse as a starting point, combining historical cases such as Terra, Iron Finance, USDC, and others to reveal the structural flaws that repeatedly appear in the DeFi ecosystem: unsustainable high yields, circular dependencies, lack of transparency, overcollateralization, oracle vulnerabilities, and comprehensive infrastructure failures under pressure.

The following is the original article:

In the first two weeks of November 2025, decentralized finance (DeFi) exposed the fundamental flaws that academia has warned about for years. The collapse of Stream Finance's xUSD, followed by Elixir's deUSD and the successive breaches of numerous synthetic stablecoins, was not just a case of poor management, but a revelation of the structural issues in the DeFi ecosystem concerning risk control, transparency, and trust mechanisms.

In the collapse of Stream Finance, what I saw was not a traditional smart contract exploit or oracle manipulation but a more alarming fact: a fundamental financial transparency deficit packaged with "decentralization." When an external fund manager lost $93 million with almost no effective oversight and triggered a $285 million cross-protocol cascade; when the entire "stablecoin" ecosystem saw a 40%-50% evaporation of total value locked (TVL) in a week while maintaining peg, we must acknowledge a basic fact: the current decentralized finance industry is making no progress.

More precisely, the current incentive mechanism is rewarding those who ignore lessons, punishing the cautious, and socializing losses when inevitable failures occur.

There is an old saying in the financial field, "If you don't know where the yield comes from, then the yield is you." When certain protocols promise an 18% return without disclosing their strategies, while the mature lending market only offers 3%-5%, then the source of this yield must inevitably be the depositors' principal.

Stream Finance's Mechanism and Risk Transmission

Stream Finance positions itself as a yield optimization protocol, promising users an annualized 18% return on USDC deposits through its yield-bearing stablecoin xUSD. Its publicized strategies include "Delta Neutral Trading" and "Hedged Liquidity Providing," terms that sound sophisticated but provide little substantive information on actual operations.

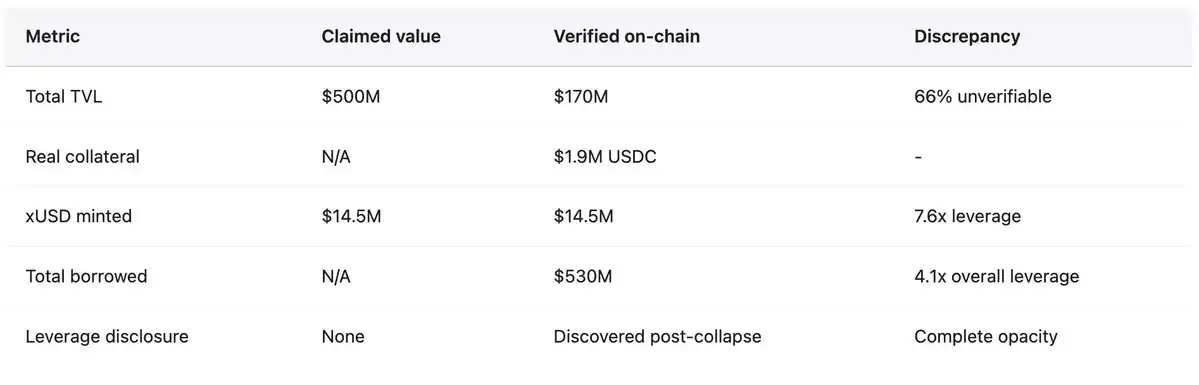

By contrast, established protocols at the time such as Aave offered an annualized yield of only 4.8% on USDC deposits, while Compound slightly exceeded 3%. When basic financial common sense should have cautioned people against a return three times the market norm, users still poured in hundreds of millions of dollars. Before the collapse, the trading price of 1 xUSD reached 1.23 USDC, reflecting the so-called compounding returns. xUSD claimed to manage assets worth as much as $382 million, but DeFiLlama data showed its peak TVL was only $200 million, meaning over 60% of assets existed in unverifiable off-chain positions.

After the collapse, Yearn Finance developer Schlagonia revealed the actual mechanism, exposing a systematic fraud disguised as financial engineering. Stream created uncollateralized synthetic assets through recursive borrowing, with the process as follows: Users deposited USDC, which Stream converted to USDT via CowSwap, then used the USDT to mint deUSD on Elixir, which was selected due to high yield incentives. Subsequently, deUSD was bridged to chains like Avalanche and deposited into lending markets to borrow USDC, completing a cycle.

Up to this point, the strategy still resembled standard collateralized borrowing and lending, but the complexity and cross-chain dependencies were concerning.

However, Stream did not stop there. It used the borrowed USDC not only for additional collateral loops but also re-minted xUSD through its StreamVault contract, causing the xUSD supply to far exceed actual collateral support. In the end, with only $1.9 million in verifiable USDC collateral, Stream minted $14.5 million xUSD, expanding the synthetic asset relative to the underlying reserve by 7.6 times. This was a form of "fractional reserve banking" behavior without reserves, regulation, or a lender of last resort.

The circular dependencies with Elixir made the structure even more fragile.

During the inflation of the xUSD supply cycle, Stream deposited $10 million USDT into Elixir, expanding the supply of deUSD. Elixir then exchanged this USDT for USDC and deposited it into Morpho's lending market. By early November, USDC deposits on Morpho exceeded $70 million, with borrowings surpassing $65 million, with Elixir and Stream being two of the major players.

Stream holds about 90% of the deUSD total supply (about $75 million), while Elixir's collateral is mainly from a loan issued by Morpho to Stream. These stablecoins are mutually collateralized, destined to collapse together. This is a form of "financial inbreeding," creating systemic fragility.

Industry analyst CBB issued a public warning on October 28: "xUSD has about $170 million in on-chain collateral, yet has borrowed about $530 million from lending protocols, with a leverage ratio of 4.1x and extremely poor liquidity of positions. This is not a yield farm but a full-fledged gamble." Schlagonia had warned the Stream team 172 days before the collapse, stating that it would take just five minutes of looking at their positions to see that failure was inevitable. These warnings were public, specific, and accurate, but ultimately overlooked by users driven by profit motives, fee-chasing curators, and protocols that tolerated the entire structure.

On November 4, Stream announced that an external fund manager had lost approximately $93 million in asset management, prompting the platform to immediately halt all withdrawals. With no redemption mechanism, panic quickly spread, and holders rushed to sell xUSD in a highly illiquid secondary market. Within hours, xUSD plummeted by 77% to around $0.23. This stablecoin, once promising stability and high returns, lost three-quarters of its value in a single trading day.

Digitally Presented Risk Transmission

According to the DeFi research firm Yields and More (YAM), the direct debt exposure related to Stream reached $285 million in the entire ecosystem, involving: TelosC loans of $123.64 million (single largest curator exposure), Elixir Network borrowing $68 million through Morpho's private treasury (65% of deUSD collateral), MEV Capital $25.42 million, of which about $650,000 in bad debt stemmed from the oracle freezing xUSD price at $1.26 when the real market price had dropped to $0.23; Varlamore $19.17 million, Re7 Labs holding $14.65 million and $12.75 million in two treasuries respectively, in addition to smaller positions by Enclabs, Mithras, TiD, and Invariant Group. Euler faces about $137 million in bad debt, with frozen funds exceeding $160 million across protocols. Researchers note that this list is not exhaustive and warn that there "may be more stablecoins and treasuries affected," as the full picture of the interconnected exposures remains unclear weeks after the collapse.

The deUSD of Elixir plummeted from 1.00 US Dollar to 0.015 US Dollar within 48 hours after concentrating 65% of its reserves in loans issued by Morpho to Stream, becoming the fastest major stablecoin collapse since Terra UST in 2022. Elixir provided a 1:1 USDC redemption for about 80% of non-Stream holders, safeguarding most of the community, but this protection came at a significant cost, with losses distributed to Euler, Morpho, and Compound. Subsequently, Elixir announced the complete termination of all stablecoin products, acknowledging that trust was irreparably broken.

A broader market response indicated systemic loss of confidence. According to Stablewatch data, yield-bearing stablecoins experienced a 40%-50% TVL drop in the week following the Stream collapse, although most still maintained their dollar peg. This meant that around $1 billion flowed out of protocols that had never faced issues, as users were unable to differentiate between sound projects and fraudulent ones, opting for full withdrawal. The entire DeFi TVL decreased by $200 billion in early November, reflecting systemic contagion risk rather than the failure of a single protocol.

October 2025: $60 Million Triggers Chain Liquidation

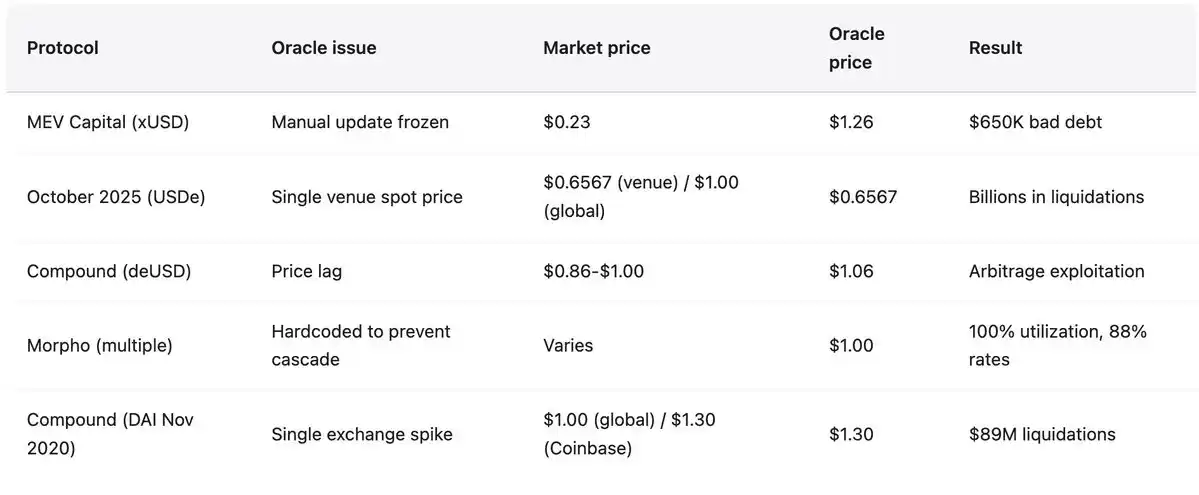

Less than a month before the Stream Finance collapse, the cryptocurrency market experienced a "precision attack" revealed through on-chain forensic analysis, rather than a typical market crash. This attack exploited well-known industry vulnerabilities and was executed at an institutional scale. On October 10-11, 2025, a carefully orchestrated $60 million sell-off triggered an oracle failure, leading to widespread chain liquidation across the DeFi ecosystem. This was not due to excessive leverage on real damaged positions but to an institutional-level failure in oracle design, replaying attack patterns recorded and disclosed since February 2020.

The attack began at 5:43 AM UTC on October 10th, where $60 million of USDe was dumped on a single trading platform. In a sound oracle system design, such behavior should have been absorbed by a multi-source price and time-weighted mechanism, with minimal impact. However, the oracle instantly devalued collateral assets (wBETH, BNSOL, and USDe) based on the manipulated spot price of the trading platform, triggering widespread liquidations. The infrastructure was instantly overwhelmed, with millions of liquidation requests flooding the system's capacity. Market makers were unable to place orders promptly due to API outages, withdrawal queues, instant liquidity evaporation, and the self-reinforcing cascade of events.

Attack Methods and Historical Precedents

An oracle faithfully reported a manipulated price on a single trading platform while other market prices remained stable. The main trading platform showed the price of USDe dropping to $0.6567, wBETH dropping to $430, while price deviations on other trading platforms were less than 30 basis points, and the on-chain pool was hardly affected. As Ethena's founder Guy Young pointed out, "During the event, over $9 billion in stablecoin collateral could be redeemed immediately," proving that the underlying assets were not affected. However, the oracle reported manipulated prices, the system settled based on these prices, positions were liquidated, and these valuations did not exist in any other markets.

This pattern mirrors the November 2020 Compound disaster, where DAI surged to $1.30 on Coinbase Pro within an hour while other markets remained at $1.00, resulting in an $89 million liquidation.

The attack surface has changed, but the vulnerabilities have not. The methods align with those of February 2020 bZx (manipulated $980,000 via a Uniswap oracle), October 2020 Harvest Finance (manipulated $24 million via Curve and triggered a $570 million run), and October 2022 Mango Markets (cross-platform manipulation to siphon $117 million), among others.

Between 2020 and 2022, there were 41 oracle manipulation attacks that stole a total of $403.2 million. Industry reactions have been slow and fragmented, with most platforms still relying heavily on spot prices and inadequate redundancy in oracles. The amplification effect shows that as the market grows, these lessons become more crucial. In the 2022 Mango Markets incident, $5 million in manipulation leveraged $117 million, amplifying it 23 times; in October 2025, a $60 million manipulation caused a massive chain reaction. The attack patterns have not become more complex, and as the system scale expands, it retains the same fundamental vulnerabilities.

Historical Patterns: Failure Cases from 2020 to 2025

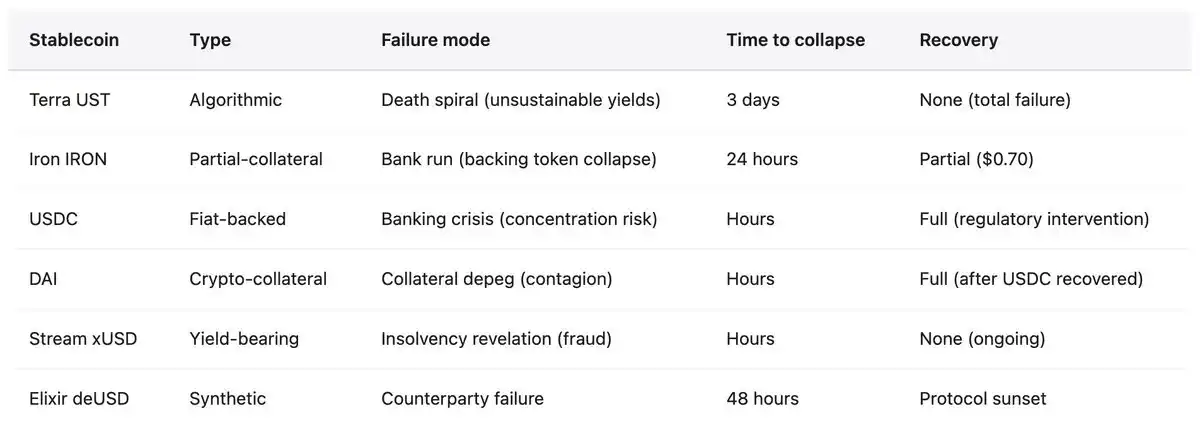

The collapse of Stream Finance is neither new nor unprecedented. Over the past five years, the DeFi ecosystem has seen repeated stablecoin failures, each time exposing similar structural vulnerabilities, yet the industry repeats the same mistakes on a larger scale. The pattern is highly consistent: algorithmic stablecoins or partially collateralized stablecoins attract deposits with unsustainable high yields, where the revenue is not from actual earnings but relies on token issuance or new fund inflows. Protocols operate in structures of excessive leverage, opaque real collateral ratios, and cyclical dependencies—protocol A supports protocol B, which in turn supports protocol A. Once any shock reveals insolvency in the underlying assets or subsidies cannot be maintained, a run begins. Users rush to withdraw, collateral values collapse, liquidation cascades trigger, and the entire structure disintegrates in a matter of days or even hours. Risk spreads to protocols that accept the failed stablecoin as collateral or hold related positions.

May 2022: Terra (UST/LUNA)

Loss: $45 billion market cap evaporated in three days. UST is an algorithmic stablecoin backed by LUNA through a seigniorage mechanism. The Anchor Protocol provides unsustainable yields of up to 19.5% on UST deposits, with around 75% of UST deposited in the protocol earning rewards. The system relied on continuous fund inflows to maintain stability. Trigger: $375 million withdrawn from Anchor on May 7, followed by massive UST sell-offs leading to destabilization. Users exiting exchanged UST for LUNA, increasing LUNA supply from 346 million to 65 trillion within three days, triggering a death spiral and near-zeroing of both tokens. The collapse not only wiped out individual investors but also led to the closure of major crypto lending platforms like Celsius, Three Arrows Capital, Voyager Digital, among others. Terra founder Do Kwon was arrested in March 2023 and faces multiple fraud charges.

June 2021: Iron Finance (IRON/TITAN)

Loss: $20 billion TVL wiped out within 24 hours. IRON partially collateralized, 75% USDC + 25% TITAN. The protocol attracted funds through incentives of up to 1700% APY. When large holders started redeeming IRON for USDC, Titan sell-offs intensified, crashing the price from $64 to $0.00000006, destroying IRON's collateral. Lesson: Partial collateralization is insufficient under pressure, and arbitrage mechanisms fail under extreme circumstances, especially when the collateral token itself enters a death spiral.

March 2023: USDC

Destabilization: Reserves of $3.3 billion trapped in a collapsed Silicon Valley bank led to a price drop to $0.87 (13% loss). This was supposed to be an "impossible event" as USDC is a "fully-backed" fiat stablecoin with regular audits. Stability resumed only after the FDIC invoked systemic risk exceptions and SVB secured deposits. Risk transmission: Triggered DAI destabilization as over 50% of its collateral was in USDC, leading to over 3400 liquidations on Aave totaling $24 million. Proof that even compliant stablecoins face concentration risks, relying on the stability of the traditional banking system.

November 2025: Stream Finance (xUSD)

Loss: $93 million direct loss, ecosystem total exposure $285 million. Mechanism: Recursive lending to create uncollateralized synthetic assets (real collateral expansion by 7.6x). 70% of funds flowed into anonymously managed off-chain strategies with no reserve proof. Current status: xUSD trading price between $0.07-$0.14 (down 87%-93% from peg), minimal liquidity, indefinite withdrawal freezes. Multiple lawsuits filed, Elixir fully exiting, industry funds massively withdrawing from yield-bearing stablecoins.

All cases presented exhibit a common failure pattern.

- Unsustainable High Yield: Terra (19.5%), Iron (1700% APY), Stream (18%) all offer returns disconnected from actual revenue.

- Circular Dependency: UST-LUNA, IRON-TITAN, xUSD-deUSD all feature a mutually reinforcing failure pattern, where the collapse of one inevitably drags down the other.

- Lack of Transparency: Terra conceals Anchor's subsidy cost, Stream hides 70% of operations off-chain, Tether has faced repeated doubts about its reserve composition.

- Partial Collateralization or Self-Issued Collateral: Relying on volatile or self-issued tokens triggers a death spiral under pressure, as the collateral value plummets right when it needs to support the most.

- Oracle Manipulation: Frozen or manipulated price feeds hinder normal liquidation, turning price discovery into a game of trust, with bad debts accumulating until the system is insolvent.

The conclusion couldn't be clearer: stablecoins are not stable. They are only "stable-seeming," until they're not, and this transformation often happens within hours.

Oracle Failure and Infrastructure Collapse

At the onset of Stream's collapse, the oracle issue was immediately exposed. As the actual market price of xUSD dropped to $0.23, many lending protocols had oracle prices hardcoded at $1.00 or higher to prevent cascading liquidations. This practice, meant to maintain stability, instead resulted in a fundamental disconnect between protocol behavior and market reality. This was not a technical glitch but a human-made policy. Many protocols opted for manual oracle updates to avoid liquidations triggered by brief fluctuations. However, when price drops reflect genuine insolvency rather than temporary pressure, this approach leads to catastrophic consequences.

The protocols faced an unsolvable dilemma:

Use real-time prices: The risk lies in being manipulated during volatility, sparking cascading liquidations, as seen in October 2025, with devastating consequences.

Use delayed prices or Time-Weighted Average Price (TWAP): Unable to address actual bankruptcy and bad debt accumulation, Stream Finance is a case in point—where the oracle showed $1.26, but the actual price was only $0.23, resulting in MEV Capital alone incurring $650,000 in bad debt.

Manual Intervention Use: Introduction of centralization, discretionary intervention, and the ability to mask bankruptcy by freezing the oracle. All three schemes have led to losses in the range of hundreds of millions to tens of billions of dollars.

Under Pressure Infrastructure Capacity

Following the infrastructure collapse of Harvest Finance in October 2020, TVL dropped from $1 billion to $599 million due to a $24 million exploit triggering user panic withdrawals. The lesson was clear: oracle systems must consider infrastructure capacity under stress events, liquidation mechanisms must have rate limits and circuit breakers, and trading platforms must maintain a redundancy capacity ten times the normal load.

However, by October 2025, this lesson had not been learned at the institutional level. When millions of accounts faced liquidation simultaneously, billions of dollars in positions were closed within an hour, order books went blank due to exhaustion of buy orders, and the system overload prevented placing orders, infrastructure failure was as complete as the oracle's. Technical solutions existed but were not implemented because they reduced normal efficiency and added costs, costs that could have been converted into profits.

If you cannot identify the source of your revenue, you are not earning revenue; you are footing the bill for someone else's earnings. This principle is not complex, yet billions of dollars are still poured into black-box strategies because people prefer to believe a comfortable lie rather than face an uncomfortable truth. The next Stream Finance is already in operation.

Stablecoins are not stable. Decentralized finance is neither decentralized nor secure. Income without a clear source is not profit but rather pillage with a ticking clock. This is not an opinion but a fact validated at great cost. The only question is whether we will take action or replay the $200 billion scenario. History suggests the latter.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.